VCOVID-19 Concerns Make 2020 3D Printer Sales Outlook Challenging

As of the end of Q1 2020, many 3D printer companies from the US, Europe, China and everywhere across the globe have rightly refocused their effort away from printer sales to producing much-needed supplies to help combat coronavirus, according to the latest by CONTEXT, the market intelligence company.

“By focusing efforts on producing much-needed medical supplies has meant a move away from the production and sale of printers towards service businesses and service-bureau infrastructure”, said Chris Connery, VP of global analysis at CONTEXT. “Coming on the back of weak shipments in Q4 2019, this refocus – and the supply-and-demand constraints expected in the weeks to come – looks to make 2020 a difficult year for 3D printer shipments.”

“While COVID-19 had not yet had an impact, global 3D printer shipments were already unseasonably weak in Q4 2019. For many manufacturers – particularly those focused on Industrial* or Design* price-class printers – this slowdown was associated with a weak automotive market, a generally weak manufacturing sector and sluggish Asian and European economies.”

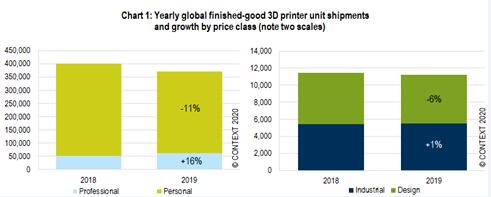

CONTEXT notes that printer shipments over the quarter saw year-on-year changes of -11% (Personal* price-class printers), +26% (Professional* printers), -22% (Design) and -23% (Industrial); the only increase being in the hot Professional category.

Over the year as a whole, there was only +1% growth in shipments of Industrial printers compared to 2018; in the Design segment, -6% fewer printers shipped; and finished-good Personal printer shipments were down by -11% as demand continued to shift to kits, sales of which are hard to quantify. Once again, the only year-on-year growth was in the Professional segment where shipments rose by +16% as many longstanding 3D printer companies returned to the space and others, previously focused on producing Personal printers, moved up into it.

Image via CONTEXT

Image via CONTEXT

In the finished-good Personal 3D printer market, 2019 was strong for established vendors such as XYZPrinting, Prusa Research, Monoprice, Anycubic and Flashforge but it was the more ill-defined kits market which drew the most industry attention. The leader in the kits space – and far-and-away the market share leader in the global 3D printer market when considering both kits and finished-goods – was China’s Creality 3D. While it was once assumed that consumer demand for DIY kits would fade away in the face of the better out-of-the-box experience offered by completed machines, self-assembly – largely catering to hobbyists – has come back into vogue in recent years. This is thanks to not just very low price points but also protectionist measures which favour the importation of parts that can be assembled locally over finished goods even though, in this case, the assembly is on an individual do-it-yourself basis rather than factory-level production. The number of DIY kits shipped in 2019 was almost twice as high as that of finished printers but, if aggregated into the annual total, sales to this nebulous market would have increased global revenues by only +9%.

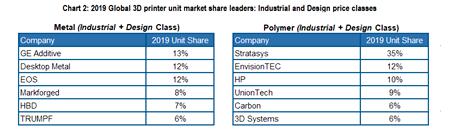

In the Design and Industrial segments – which collectively accounted for over 78% of all 3D printer sales revenue – aggregate shipments were down -3% for 2019. Although metal 3D printer shipments were up +4% on the previous year, with steady growth seen in emerging technologies like material extrusion and directed energy deposition, there was a -10% decline in those of mainstream powder bed fusion printers. Market leaders GE Additive and EOS were joined in the top 5 by Desktop Metal and Markforged (both of which offer material extrusion based solutions) and newcomer HBD which performed strongly in China, its domestic market. Overall shipments of Industrial and Design polymer printers fell by -5% compared to 2018 but certain vendors, including HP and UnionTech, saw excellent growth. Stratasys remained the market leader in terms of unit volumes even though annual shipments dropped by -12% in 2019.

Image via CONTEXT

Image via CONTEXT

Forecasts for 2020, based on information available as of 23 March, show printer manufacturers are now assessing, on a daily basis, the impacts of a disrupted supply chain and uneven human productivity on both their own ability to produce hardware and the end-markets to which they cater. In recent years, vendors have typically begun with a bullish outlook and slowly adjusted their shipment outlook over the year. Currently, however, vendors are offering only informal/high-level forecasts: most are beginning 2020 with a negative outlook and anticipating they will recover as business begins again once the global pandemic subsides. While each printer class caters to different users, many of the key end-markets (such as the dental, aerospace, automotive, consumer product, orthopaedics and education markets) are negatively affected by global work closures and slow-downs. On the supply side, key components for printers, as for many other electronic goods, come from China, the region impacted first by the pandemic. As a result of the uncertainty, hardware vendors are now thinking in terms of weeks and quarters rather years, and current aggregate forecasts show the Industrial and Design segments are set to see shipment declines of -4% from 2019 to 2020 even taking into consideration a recovery in the 2nd half of the year.

In the Industrial market – which accounted for 68% of global 3D printer hardware revenues 2019 – shipments in the second half of 2019 were slow, even though this is usually the strongest part of the year, and the outlook for 2020 was, therefore, already challenging. Taking into account both these negative headwinds and the supply-and-demand challenges associated with global reactions to the coronavirus, this segment hopes to see a slide of only -2% in printer shipments in 2020 after its 5-year CAGR of +14% and anticipates a rolling recovery by region, starting with the East.

As the pandemic comes under control and economies return to normal, there is great potential for the 3D printer market since the ability of the technology to assist with the immediate needs of the medical community have showcased its quick-turn capabilities worldwide. Responses to the pandemic are also demonstrating that leveraging 3D printing for local production, instead of relying on complex multinational supply chains, has the potential to help many companies mitigate future risk.

Image via CONTEXT

Image via CONTEXT

* 3D printer price classes: Industrial ≥ $100K, Design = $20K–$100K, Professional = $2.5K–$20K, Personal ≤ $2.5K (excludes DIY kit printers)

Source: CONTEXT

Recent Comments