Key 3D Printer Markets on Track for Double-Digit Shipment Growth in The Second Half of 2019

Industrial, Design and Professional price class printer shipments set to rise 14%, 13% and 15% respectively in 2019 as Personal class struggles

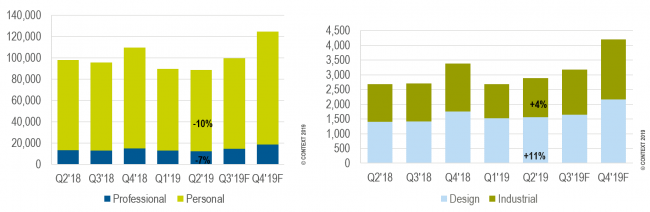

While shipments of 3D printers in the Personal* price class struggled to remain flat in the first half of 2019, the other three major price classes – Professional, Design and Industrial – saw encouraging global unit shipment growth. CONTEXT expects double-digit unit shipment growth for the year as a whole in all three of these segments with different outlooks for each of the disparate sub-markets.

![]() Personal price class

Personal price class

Defined by having an entry-level price point (below $2,500), this class of 3D printers has now seen six consecutive quarters of declining sales. Projections for the remainder of the year show that the class may struggle to see flat year-on-year shipment totals after a fall of -10% in Q2 2019. With no signs of emerging geographies, and sales yet to take root outside the education and hobby markets, many vendors are now completely shifting their focus to the Professional class.

![]() Professional price class

Professional price class

On a trailing twelve months (TTM) basis, this class – along with the Industrial class – has seen the greatest growth: with unit shipments up +8% and revenues rising +37% over the last year it is now a hot sector. While the dental market has embraced many modes of 3D printing using machines at a range of price points, sales of Professional printers have been exceptionally strong in recent quarters – exemplified by strong shipments of 3D Systems’ Figure-4/NextDent platform and EnvisionTEC’s One line. Market leaders such as 3D Systems and Stratasys have renewed their focus on this Professional price class, having left the likes of Ultimaker and Formlabs to dominate over the last few years The segment saw a short- term downturn in Q2 2019 with shipments falling by -7% year-on-year, but this was more a supply-chain issue than due to reduced demand. Although one of the segment leaders, Formlabs, has recently been struggling a little to bring new products to market, shipments started to get back on track in Q3.

Chart 1: Global 3D printer shipments by price class showing Y/Y change (note two scales)

Unit sales in this segment have long been dominated by three of the oldest players in the market (Stratasys, 3D Systems and EnvisionTEC) but recent quarters have seen HP enter the field and contribute to an 11% rise in shipments in Q2 2019 – and an even stronger rise in printer revenues of +26% . HP’s new colour 3D printers performed especially well in this period.

Unit sales in this segment have long been dominated by three of the oldest players in the market (Stratasys, 3D Systems and EnvisionTEC) but recent quarters have seen HP enter the field and contribute to an 11% rise in shipments in Q2 2019 – and an even stronger rise in printer revenues of +26% . HP’s new colour 3D printers performed especially well in this period.

![]() Industrial price class

Industrial price class

Industrial price-class printer shipments were up just +4% in Q2 2019 and only +5% in 1H 2019 but, historically, over 30% of this category’s shipments come in the fourth quarter. Key verticals such as the European automotive sector are currently weak – as evidenced by the shipment of -18% fewer metal powder bed fusion printers in Q2 2019 than in the year before – and many are pointing to slow sales into this market as a key issue. However, other verticals are still strong and the outlook for the year remains positive. Shipments of Industrial class printers in the Chinese domestic market were particularly strong in 1H 2019, and the new sub-class of lower-priced metal 3D printing solutions from the likes of Desktop Metal and Markforged have also buoyed this class this year.

Bottom-up forecasts for 2H 2019 project that strong Q4 shipments will yield double-digit unit shipment growth in the Industrial, Design and Professional classes with the Professional class poised for the strongest annual growth of +15%. The Industrial and Design markets collectively account for 79% of current global printer revenues with 59% of total revenues being amassed by the top five companies in this aggregated group.

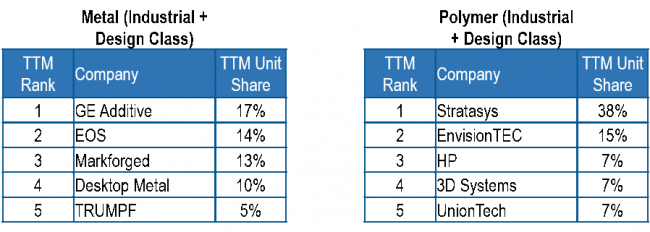

Table 1: Combined Industrial + Design class 3D printers: global TTM (Q2’18-Q2’19) unit shipment share by material and vendor

* 3D-printer segment by price class: Industrial ≥ $100K, Design = $20K–$100K, Professional = $2.5K–$20K, Personal ≤ $2.5K

Source: CONTEXT

Recent Comments